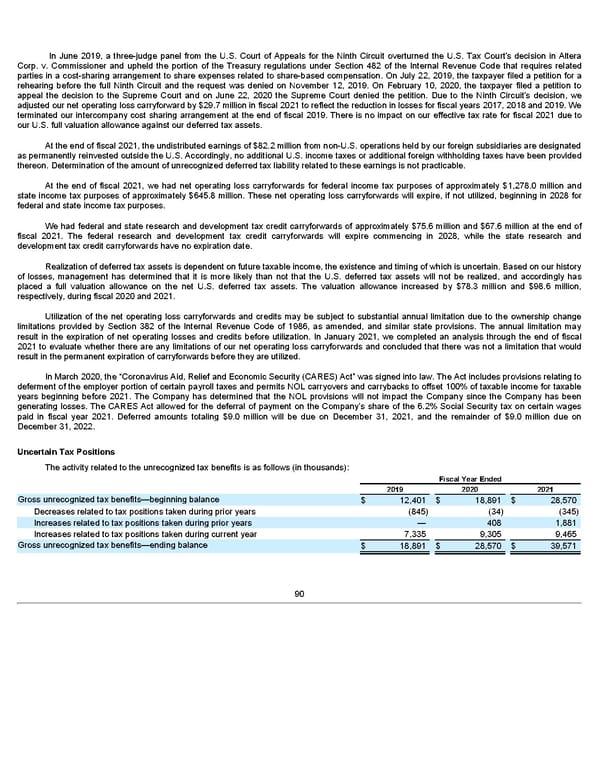

In June 2019, a three-judge panel from the U.S. Court of Appeals for the Ninth Circuit overturned the U.S. Tax Court's decision in Altera Corp. v. Commissioner and upheld the portion of the Treasury regulations under Section 482 of the Internal Revenue Code that requires related parties in a cost-sharing arrangement to share expenses related to share-based compensation. On July 22, 2019, the taxpayer filed a petition for a rehearing before the full Ninth Circuit and the request was denied on November 12, 2019. On February 10, 2020, the taxpayer filed a petition to appeal the decision to the Supreme Court and on June 22, 2020 the Supreme Court denied the petition. Due to the Ninth Circuit's decision, we adjusted our net operating loss carryforward by $29.7 million in fiscal 2021 to reflect the reduction in losses for fiscal years 2017, 2018 and 2019. We terminated our intercompany cost sharing arrangement at the end of fiscal 2019. There is no impact on our effective tax rate for fiscal 2021 due to our U.S. full valuation allowance against our deferred tax assets. At the end of fiscal 2021, the undistributed earnings of $82.2 million from non-U.S. operations held by our foreign subsidiaries are designated as permanently reinvested outside the U.S. Accordingly, no additional U.S. income taxes or additional foreign withholding taxes have been provided thereon. Determination of the amount of unrecognized deferred tax liability related to these earnings is not practicable. At the end of fiscal 2021, we had net operating loss carryforwards for federal income tax purposes of approximately $1,278.0 million and state income tax purposes of approximately $645.8 million. These net operating loss carryforwards will expire, if not utilized, beginning in 2028 for federal and state income tax purposes. We had federal and state research and development tax credit carryforwards of approximately $75.6 million and $67.6 million at the end of fiscal 2021. The federal research and development tax credit carryforwards will expire commencing in 2028, while the state research and development tax credit carryforwards have no expiration date. Realization of deferred tax assets is dependent on future taxable income, the existence and timing of which is uncertain. Based on our history of losses, management has determined that it is more likely than not that the U.S. deferred tax assets will not be realized, and accordingly has placed a full valuation allowance on the net U.S. deferred tax assets. The valuation allowance increased by $78.3 million and $98.6 million, respectively, during fiscal 2020 and 2021. Utilization of the net operating loss carryforwards and credits may be subject to substantial annual limitation due to the ownership change limitations provided by Section 382 of the Internal Revenue Code of 1986, as amended, and similar state provisions. The annual limitation may result in the expiration of net operating losses and credits before utilization. In January 2021, we completed an analysis through the end of fiscal 2021 to evaluate whether there are any limitations of our net operating loss carryforwards and concluded that there was not a limitation that would result in the permanent expiration of carryforwards before they are utilized. In March 2020, the “Coronavirus Aid, Relief and Economic Security (CARES) Act” was signed into law. The Act includes provisions relating to deferment of the employer portion of certain payroll taxes and permits NOL carryovers and carrybacks to offset 100% of taxable income for taxable years beginning before 2021. The Company has determined that the NOL provisions will not impact the Company since the Company has been generating losses. The CARES Act allowed for the deferral of payment on the Company’s share of the 6.2% Social Security tax on certain wages paid in fiscal year 2021. Deferred amounts totaling $9.0 million will be due on December 31, 2021, and the remainder of $9.0 million due on December 31, 2022. Uncertain Tax Positions The activity related to the unrecognized tax benefits is as follows (in thousands): Fiscal Year Ended 2019 2020 2021 Gross unrecognized tax benefits—beginning balance $ 12,401 $ 18,891 $ 28,570 Decreases related to tax positions taken during prior years (845) (34) (345) Increases related to tax positions taken during prior years — 408 1,881 Increases related to tax positions taken during current year 7,335 9,305 9,465 Gross unrecognized tax benefits—ending balance $ 18,891 $ 28,570 $ 39,571 90

Annua lReport Page 89 Page 91

Annua lReport Page 89 Page 91